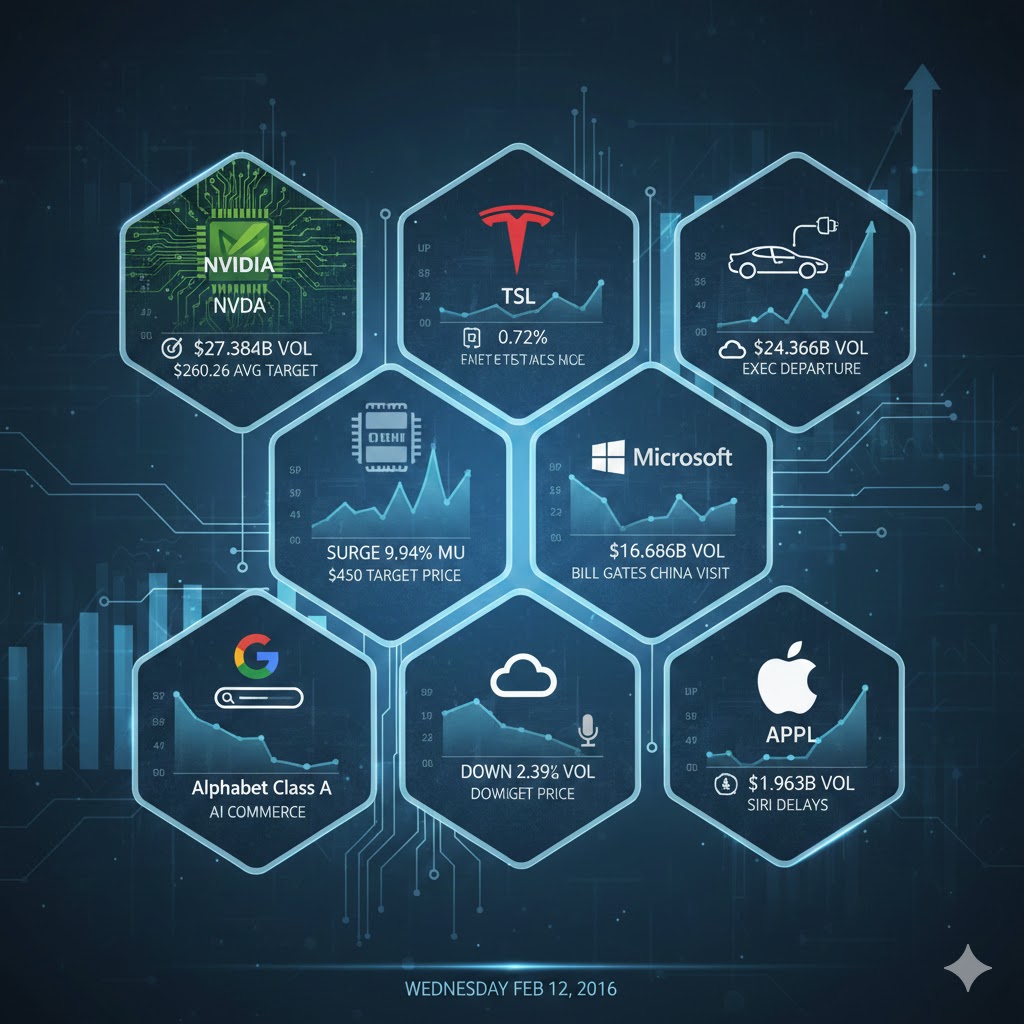

The No. 1 most actively traded U.S. stock on Wednesday was Nvidia(NASDAQ:NVDA), which closed up 0.80% with $27.384 billion in trading volume.

UBS raised its target price on Nvidia from $235 to $245.

In its latest report, Goldman Sachs lifted its earnings forecast for Nvidia’s fiscal fourth quarter of 2026 and maintained a $250 price target, emphasizing that revenue visibility for 2027 will be a key catalyst. Institutional ratings show that more than 90% of analysts assign a “Buy” or “Overweight” rating, with an average target price of $260.26, reflecting market optimism about AI computing demand. However, Goldman also warned of risks such as a slowdown in AI infrastructure investment and intensifying competition.

The No. 2 most actively traded stock was Tesla (NASDAQ:TSLA), which rose 0.72% on trading volume of $24.366 billion.

According to reports, Tesla Vice President Raj Jegannathan announced on LinkedIn on February 9 local time that he was leaving the company, ending his 13-year tenure. This marks the latest departure in a wave of executive exits from companies under Elon Musk. Previously, several core executives at Tesla and xAI had also stepped down.

Jegannathan wrote, “It’s not easy to summarize 13 years in one post. My journey at Tesla has been a continuous evolution. As I leave, I do so with gratitude and excitement for what lies ahead.”

The No. 3 most actively traded stock was Micron Technology (NASDAQ:MU), which surged 9.94% on trading volume of $19.165 billion.

On Wednesday, Morgan Stanley raised its target price on the stock from $350 to $450 while maintaining an “Overweight” rating. The new target is above Micron’s Wednesday closing price of $410.34 and aligns with the broadly bullish consensus among analysts. Public data show that the stock’s average analyst rating stands at 1.56 (Strong Buy).

In addition, during a speech at the Wolfe Research conference, Micron addressed rumors that it “might miss out on Nvidia’s new HBM4 orders,” stating that the supply-demand imbalance, with capacity in short supply, is expected to persist at least through 2028. The clarification helped lead a strong rebound in shares of several leading memory manufacturers.

The No. 4 most actively traded stock was Microsoft (NASDAQ:MSFT), which fell 2.15% on trading volume of $16.686 billion.

According to media reports, Bill Gates, chairman of the Gates Foundation, made a surprise appearance in Zhangjiang, Shanghai, on the evening of February 11 to attend an event titled “Action Creates Hope.”

This visit marked Gates’ return to China approximately two and a half years after his previous trip in June 2023.

In an interview, Gates directly addressed the controversy surrounding his relationship with Jeffrey Epstein. He clarified, “Between 2011 and 2014, I did have several dinners with Epstein, but there is really nothing new to add about that. I never had contact with any victims, nor did I ever visit his island.”

The No. 5 most actively traded stock was Alphabet Class A (NASDAQ:GOOGL), which declined 2.39% on trading volume of $14.066 billion.

According to reports, Google is introducing a new feature that allows consumers to purchase products directly when receiving AI-powered answers through its search engine and Gemini chatbot. This initiative is part of a broader strategy to monetize user engagement with artificial intelligence more directly.

In a letter to the advertising industry on Wednesday, the company said that its AI mode in Google Search is testing new ad formats that allow retailers and other advertisers to showcase products. Google also stated that users can now purchase items from Etsy and Wayfair directly within Gemini. The newly added “Direct Offers” feature in AI mode will enable brands to provide discounts to potential shoppers.

The No. 6 most actively traded stock was Apple (NASDAQ:AAPL), which rose 0.67% on trading volume of $13.963 billion.

Well-known technology journalist Mark Gurman reported that Apple’s long-planned upgrade to its Siri voice assistant has encountered setbacks in recent weeks of testing, which could delay the release of several highly anticipated features.

According to sources familiar with the matter, Apple had originally planned to introduce these new features in iOS 26.4, scheduled for release in March, but is now considering spreading them across future versions.

This means that at least some of the features could be postponed until iOS 26.5, expected in May, or even until iOS 27, set for release in September.