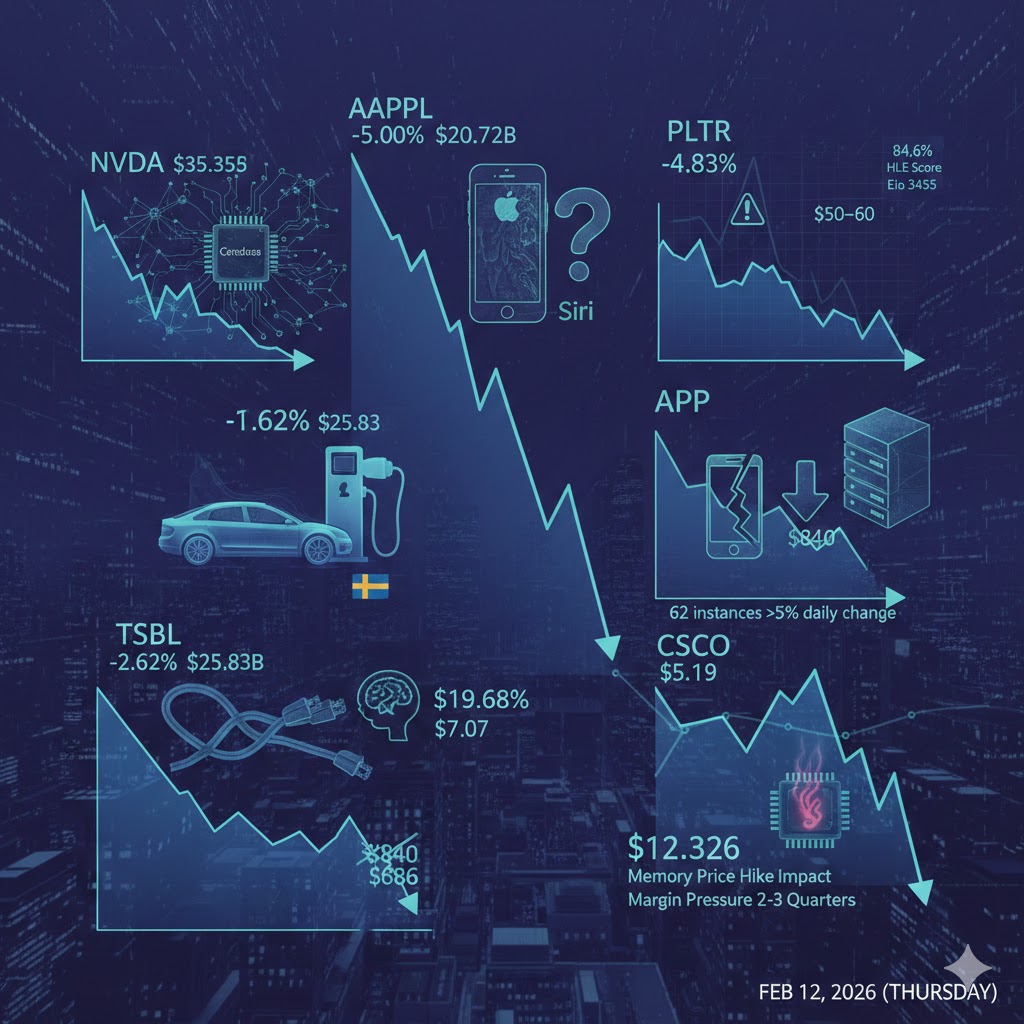

The top stocks to sell by trading volume: NVIDIA (NASDAQ:NVDA) closed down by 1.64%, with a trading volume of $35.35 billion. According to reports, OpenAI launched its first AI model powered by the chip of NVIDIA’s competitor, Cerebras. The report states that OpenAI released its first AI model based on semiconductor startup Cerebras Systems’ chip, called GPT-5.3-Codex-Spark. This model is a lightweight but faster version of its latest code automation software, Codex, designed to compete with companies like Alphabet’s Google and Anthropic in the AI programming assistant market.

Second place: Tesla (NASDAQ:TSLA) closed down by 2.62%, with a trading volume of $25.83 billion. According to Teslarati, Tesla’s supercharging stations in Sweden remain offline due to a dispute with the IF Metall union. The Swedish administrative court rejected Tesla’s appeal to force the connection of its charging stations to the grid, causing the station in Ljungby to remain idle for nearly two years since its construction. The court ruled that the union strike at Tesla’s Swedish stations was a reasonable reason for the delay. The Ljungby supercharging station is one of the first to be refused grid access following a strike initiated by IF Metall in late 2023, involving local electricians from the Seko union.

Third place: Apple (NASDAQ:AAPL) closed down by 5%, marking its largest single-day drop since early April 2025, with a trading volume of $20.72 billion. Reports suggest that Apple’s long-awaited upgrade to its Siri virtual assistant has encountered delays. Tech journalist Mark Gurman reported that Apple’s much-anticipated Siri upgrade faced issues during recent tests, and several expected features might be postponed. Apple originally planned to include these features in the upcoming iOS 26.4 release in March, but now considers rolling them out in future versions, possibly as late as iOS 26.5 in May or iOS 27 in September. This marks the second major delay since the Siri upgrade was announced in 2024.

Additionally, Apple is facing scrutiny over political bias on its news platform. The Chairman of the U.S. Federal Trade Commission, Andrew Ferguson, has urged Tim Cook to investigate potential political bias in Apple’s news operations. Ferguson posted on X, claiming that Apple News systematically prioritizes articles from left-wing media while suppressing conservative-leaning content.

Sixth place: Google-A (NASDAQ:GOOGL) closed down by 0.63%, with a trading volume of $14.79 billion. On Thursday, February 12, Google announced an upgrade to Gemini 3 Deep Think, claiming that the new model achieved breakthrough results across several industry benchmarks, including a score of 84.6% on the “Humanity’s Last Exam” (HLE) and ARC-AGI-2 tests, as verified by the ARC Prize Foundation. On the competitive programming platform Codeforces, Gemini 3 Deep Think scored an Elo rating of 3455.

Ninth place: Palantir (NYSE:PLTR) closed down by 4.83%, with a trading volume of $9.54 billion. The famous investor Michael Burry issued a warning, predicting that Palantir’s stock would drop by nearly 60%. Palantir announced that it had received a major authorization from the U.S. Defense Information Systems Agency (DISA). However, Burry expressed caution, suggesting that the stock was facing a significant technical crash, with the next support level at $80, and the “landing zone” potentially falling between $50 and $60.

Twelfth place: Applovin (NASDAQ:APP) closed down by 19.68%, with a trading volume of $7.07 billion. The stock has fallen more than 45% this year. UBS analysts downgraded their target price for the company ahead of its Q4 earnings report. The analysts lowered the target price significantly from $840 to $686, while maintaining a “Buy” rating. This adjustment came right before AppLovin’s earnings report, sending a signal to investors that contributed to the sell-off before the official results were published. Analysts pointed out that AppLovin’s stock has been extremely volatile, with 62 instances in the past year where its daily price change exceeded 5%. This recent drop suggests that the market believes this information is noteworthy but does not significantly alter the business outlook.

Seventeenth place: Cisco (NASDAQ:CSCO) closed down by 12.32%, with a trading volume of $5.19 billion. Cisco’s comments about the impact of memory price increases put pressure on tech stocks, with the company’s stock suffering its largest single-day drop since May 19, 2022, falling by 13.7%. The continued surge in memory prices has hit Cisco hard. The company disclosed that the recent quarter’s memory price hikes had negatively affected its gross margin. Cisco CEO Chuck Robbins noted during an earnings call that the company had implemented several measures to address the rising prices, including raising prices on certain products and renegotiating contracts with channel partners and customers. Robbins expressed confidence that Cisco would manage these challenges more effectively than its peers. Mizuho Securities analyst Jordan Klein pointed out that Cisco might face two to three quarters of margin pressure, and its weaker guidance poses “substantial risks” to companies like HPE (NYSE:HPE) and Dell (NYSE:DELL), as well as Arista Networks (NYSE:ANET).

On December 4, 2025, Hewlett Packard Enterprise (NYSE: HPE) released its Fiscal Year 2025 Fourth Quarter Earnings, providing a detailed snapshot of the company’s performance during a year marked by sizeable acquisitions, aggressive portfolio reshaping, fluctuating demand for AI‑optimized servers, and continued investments in cloud and networking technologies. The KR stock press release HPE Financial Report showcased record revenue and profit expansion alongside mix shifts and cost discipline — but also highlighted areas of softness and timing challenges in key segments such as AI servers and hybrid cloud. HPE’s results have implications not only for its near‑term financial performance and HPE stock price movements, but also for the company’s strategy in deploying its technology stack into hybrid cloud, AI, and networking markets.

In this deep analytical report, we explore the HPE Financial Report line by line, dissect segment‑level performance, analyze trends underlying revenue and profitability, and assess how business strategy, product positioning, and market development initiatives could influence HPE’s future revenue and earnings. We conclude with a thoughtful HPE stock outlook rooted in the company’s financial momentum and market dynamics — without offering specific investment advice.

I. Executive Summary — The Fourth Quarter Narrative

For the three months ended October 31, 2025, HPE reported:

Revenue of $9.7 billion, up 14% year‑over‑year — a record quarterly total.

Gross margin expansion of 270–550 basis points, reflecting better pricing and portfolio mix.

Non‑GAAP diluted EPS of $0.62, exceeding prior guidance and expectations.

Record free cash flow generation, with approximately $1.9 billion reported.

Continued capital returns to shareholders of about $271 million via dividends and repurchases.

Strong growth in annualized revenue run rate (ARR) to $3.2 billion — a 60%‑plus jump, driven by services and subscription offerings.

Despite solid non‑GAAP performance, GAAP diluted EPS was only $0.11, reflecting one‑time items and accounting adjustments associated with acquisitions and intangible assets.

Segment performance was mixed, with server revenue down ~5% and hybrid cloud revenue down ~12%, while networking revenue surged ~150% year‑over‑year.

These high‑level metrics reflect both the strength and the growing pains of HPE’s transformation: a portfolio increasingly weighted toward high‑growth networking and services, but still navigating uneven demand in legacy servers and cloud services, and absorbing acquisition integration costs.

II. Total Revenue Trends and Underlying Drivers

A. Revenue Growth Across the Enterprise Portfolio

HPE’s $9.7 billion in Q4 2025 revenue marked a meaningful +14% annual increase, driven by expansion across multiple high‑growth segments and the contribution from the Juniper Networks acquisition which closed earlier in the fiscal year. This acquisition — designed to bolster HPE’s networking and security capabilities — has materially altered the company’s revenue mix and growth profile.

The company’s growth in revenue was not uniform:

Networking segment revenue nearly tripled (+150%), illustrating the impact of Juniper and strong market demand for secure connectivity solutions, including campus, branch, and data center networking products.

Server revenue declined by approximately 5% year‑over‑year — reflecting timing delays in AI server shipments and softer demand in some geographies.

Hybrid cloud revenue decreased about 12%, pointing to challenges in that part of the portfolio as customers delayed deployments or shifted workloads.

Financial services revenue remained relatively stable, with modest single‑digit declines, but improved profitability margins.

This revenue divergence highlights a broader pivot within the company: networking and subscription/ARR growth are driving the fastest momentum, while traditional server and cloud businesses are contending with timing and demand variability.

B. Annualized Revenue Run Rate (ARR) and Recurring Streams

One of the most widely discussed metrics from the earnings release was the jump in ARR — to $3.2 billion, up ~62–63% year‑over‑year. This metric captures annualized subscription and consumption services revenue — including HPE’s GreenLake consumption‑based cloud offerings — and reflects accelerating customer adoption of recurring services.

ARR growth signifies a structural shift toward more stable, predictable revenue streams. As enterprises increasingly adopt as‑a‑service models for infrastructure and hybrid cloud management, recurring revenue helps smooth the traditional volatility associated with product sales cycles like servers and hardware appliances.

III. Profitability and Margin Analysis

A. Gross and Operating Margins

HPE achieved strong margin expansion in Q4:

GAAP gross margin improved to 33.5%, up roughly 270 basis points year‑over‑year.

Non‑GAAP gross margin climbed to 36.4%, a substantial 550 basis point rise.

Gross profit improvements were attributed to a favorable product mix — with networking and high‑margin services gaining share — and disciplined pricing strategies across units.

Margin uplift in a technology hardware and services company is significant; it suggests that HPE is not only growing revenue but capturing more value per dollar of sales.

B. Earnings Per Share (EPS) Dynamics

Despite the revenue and margin growth, GAAP diluted net EPS was modest at $0.11, down from the prior year. This relatively low GAAP earnings number reflects several one‑time and accounting items — including amortization of intangible assets related to recent acquisitions, stock‑based compensation, and other adjustments.

However, investors often focus on non‑GAAP diluted EPS — a metric intended to strip out unusual or non‑recurring items — which rose to $0.62, above guidance ranges. This suggests that underlying operational performance did improve, even if GAAP figures were muted by accounting treatments.

IV. Segment‑Level Performance and Strategic Implications

A detailed look at HPE’s major business lines reveals nuances that will influence future revenue trajectory and strategic emphasis:

A. Networking: A Growth Engine

The networking segment’s explosive revenue growth (~150%) was the standout story in the quarter. Fueled by the integration of Juniper Networks, this unit now boasts significantly greater scale and capability in routing, switching, wireless networking, and integrated security solutions.

This segment’s expansion has multiple strategic implications:

Cross‑Sell and Portfolio Depth: Combining HPE’s existing Aruba networking portfolio with Juniper’s routing and enterprise networking stack creates broader cross‑sell opportunities, especially in hybrid IT environments.

High‑Value Market Position: Secure, AI‑ready networking solutions are increasingly a priority as enterprises invest in digital transformation, IoT‑enabled operations, and edge‑to‑cloud interoperability.

Networking’s profitability — with operating margins near 23% — not only boosts near‑term earnings but also counters the slower parts of the business.

B. Servers and AI Workloads — Timing Challenges

HPE’s server revenue retreat (~5%) reflects the shifting cadence of enterprise spending on AI‑optimized hardware and other high‑performance computing infrastructure. Reuters reported that AI server sales were “lumpy” and timing‑dependent, as some major customers deferred orders to later in the fiscal year.

The server business remains critical to HPE’s strategic positioning for AI and hybrid cloud workloads, but this quarter underscores how timing differences — particularly with large sovereign and hyperscale clients — can distort reported results.

C. Hybrid Cloud Segment Weakness

The 12% dip in hybrid cloud revenue highlights competitive pressures from major cloud hyperscalers, tightening IT budgets among customers, and slower conversion in some segments.

However, this weakness might also reflect a timing issue rather than structural decay: many customers evaluate hybrid cloud spend on longer decision cycles, and demand can be lumpy quarter to quarter. HPE’s continued investment in GreenLake and other cloud services suggests leadership is focused on improving this segment’s performance over the long term.

D. Financial Services and Return on Equity

HPE’s Financial Services revenue was largely flat, with modest operating margin improvements and a notable uptick in return on equity. This reflects stable leasing and financial products revenue tied to enterprise hardware and solutions deployments.

While not the largest revenue contributor, Financial Services plays a strategic role in accelerating customer adoption by lowering upfront costs for complex IT solutions.

V. Operational Efficiency and Cost Management

A theme throughout the HPE Financial Report and related analyst commentary has been operational discipline. HPE has been streamlining spending, simplifying its portfolio, and executing cost‑reducing initiatives while integrating major acquisitions like Juniper.

Free cash flow generation of roughly $1.9 billion was a highlight of the quarter, exceeding expectations and reinforcing the company’s ability to generate cash even as it invests in growth initiatives.

Operational discipline matters more in a capital‑intensive business with hardware, services, and software components. Efficient cash conversion — coupled with focused R&D — positions HPE to fund innovation while maintaining financial flexibility.

VI. Outlook and Fiscal 2026 Guidance

HPE’s guidance for Fiscal 2026 — reaffirmed on December 4, 2025 — reflects both confidence and caution:

Revenue growth in the range of 17%–22%, unchanged from prior guidance, signaling strong momentum across core business areas.

Non‑GAAP operating profit growth of 32%–40%, suggesting improved leverage as costs are managed and higher‑margin segments expand.

Raised guidance for non‑GAAP diluted net EPS (to $2.25–$2.45) and GAAP diluted net EPS ($0.62–$0.82) reflects confidence that earnings will scale with revenue and margin expansion.

Increased free cash flow guidance midpoint to $1.7–$2.0 billion, emphasizing continued cash generation capacity.

Interestingly, HPE’s forecast for the first quarter of FY2026 calls for slightly softer revenue than analyst estimates, primarily due to expected timing deferrals in AI server sales. Nonetheless, the company remains committed to long‑term growth and profitability expansion.

VII. External Market and Competitive Dynamics

HPE operates in a fiercely competitive technology landscape where macroeconomic trends, enterprise IT budgets, and competitive pressures shape performance:

Server markets are influenced by CIO priorities for AI and high‑performance computing, with competition from Dell Technologies, Lenovo, Super Micro, and cloud‑native alternatives.

Hybrid Cloud competes with hyperscale cloud providers such as AWS, Azure, and Google Cloud, requiring HPE to differentiate its on‑premises and consumption‑based offerings.

Networking markets now pivot on secure, AI‑driven solutions, and HPE’s expanded networking portfolio post‑Juniper positions it to capture meaningful share.

GreenLake and as‑a‑service models align with CIO preferences for operational flexibility, making recurring revenue expansion a strategic priority.

These dynamics underscore that HPE’s performance — and the pathway for HPE stock price appreciation — is contingent both on execution and market receptivity to its value propositions.

VIII. Current HPE Stock Price Snapshot and Valuation Context

As of early January 2026, HPE stock price was approximately $22.17 per share, with a 52‑week range of about $11.97 to $26.44, indicating both recent volatility and an overall upward trajectory over the past year.

From a valuation standpoint:

Analysts tracking HPE stock note a potential longer‑term target of around $26.13, suggesting modest upside from current levels.

Dividend yield is around 2.4%–2.6%, contributing to income‑oriented investor appeal.

Price‑to‑earnings ratios remain atypical owing to accounting variations in EPS, but forward expected growth rates in EPS and ARR expansion align with higher valuation multiples than in prior years.

While HPE stock does not trade exceptionally cheaply on a trailing basis due to earnings normalization effects, forward metrics — particularly non‑GAAP EPS growth and recurring revenue acceleration — underpin a valuation narrative that emphasizes growth at a reasonable price.

IX. Strategic Drivers and Long‑Term Considerations

Looking ahead, several strategic themes could influence HPE’s revenue and earnings trajectory — and by extension, the HPE stock valuation discourse:

A. AI and High‑Performance Infrastructure Demand

HPE’s exposure to AI‑optimized servers and supercomputing solutions (including its Cray portfolio) positions it well for long‑term growth as enterprises and public sector clients invest heavily in data‑intensive computing.

B. Hybrid and Edge Cloud Adoption

GreenLake’s ARR expansion and consumption‑based services reflect secular trends toward hybrid cloud deployments, which can yield higher lifetime customer value and revenue predictability.

C. Networking and Security Expansion

The integration of Juniper and deeper penetration of secure networking — including campus, branch, and data center solutions — enhances HPE’s addressable market and cross‑sell opportunities.

D. Operational Leverage and Cost Management

Continued discipline in cost structure, guided by structural cost management initiatives and portfolio optimization, underpin margin resilience and cash flow expansion.

E. Capital Returns and Balance Sheet Health

Free cash flow strength and shareholder return programs (dividends and repurchases) support confidence in underlying earnings power while enabling strategic flexibility.

X. Conclusion: Interpreting HPE’s Financial Performance and Strategic Positioning

The December 4, 2025 HPE Financial Report encapsulates a pivotal moment in Hewlett Packard Enterprise’s evolution: one marked by record revenue, shifting segment dynamics, and strategic investments that are reshaping the company’s future. While certain product lines such as servers and hybrid cloud experienced headwinds related to timing and macro trends, networking and recurring revenue growth stand out as engines of future profitability. Coupled with improved margins and robust free cash flow, HPE’s foundational elements point toward a sustainable growth pattern that aligns with the company’s revised guidance for fiscal 2026.

For market participants watching HPE stock, the narrative is multifaceted: short‑term revenue timing and segment variability may temper near‑term movements, but structural shifts toward recurring revenue, services, and high‑growth networking bode well for future earnings stability and potential multiple expansion. HPE’s strategic repositioning — including integration of key acquisitions like Juniper Networks — underscores confidence in its ability to compete effectively across next‑generation enterprise IT infrastructure domains.

Overall, the HPE Financial Report reveals a company that is moving beyond legacy tech cycles into a more diversified, software‑ and services‑oriented future — a transformation that should resonate with long‑term investors and analysts alike.