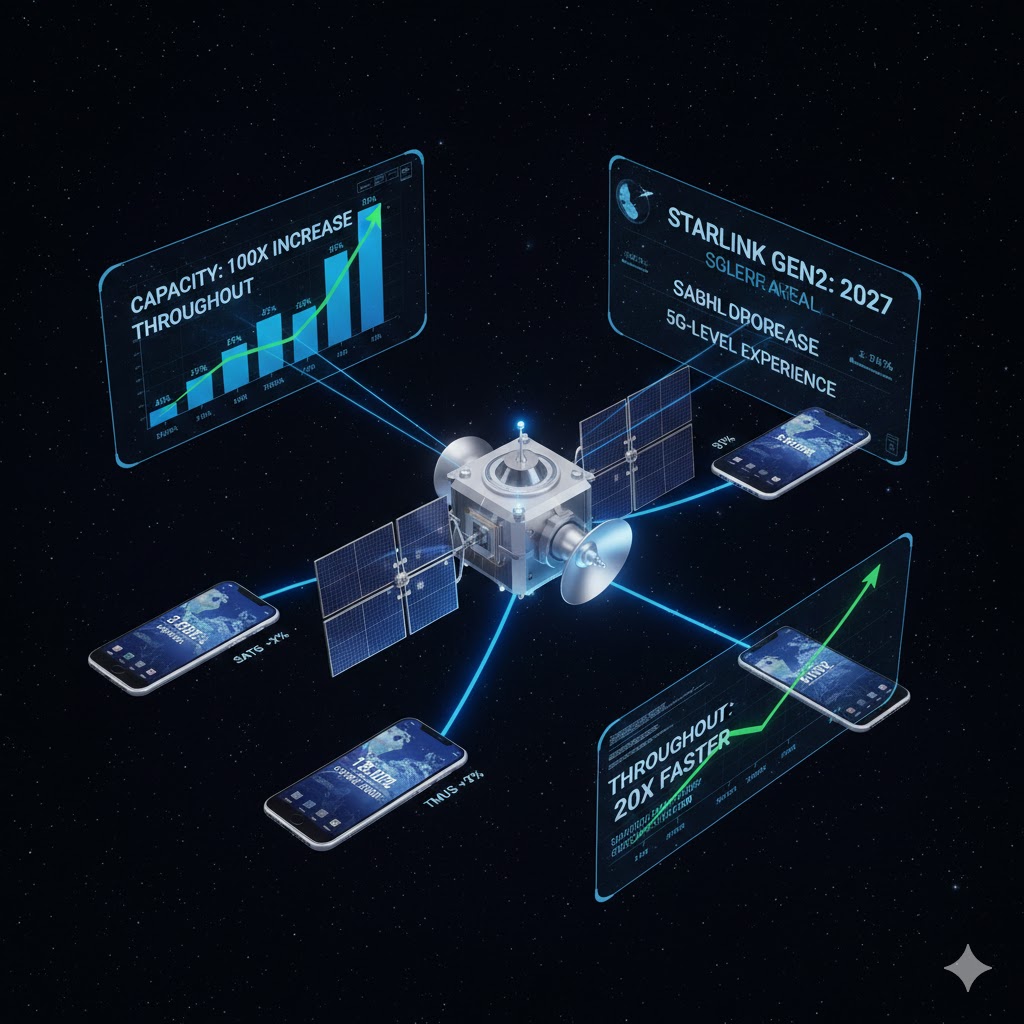

In recent filings submitted to the Federal Communications Commission (FCC), SpaceX revealed plans to launch its second-generation cellular Starlink system in 2027. The project aims to deliver “substantially enhanced” satellite-to-cell services, providing a connectivity experience comparable to terrestrial 5G networks.

This technological leap is closely tied to a pivotal acquisition finalized last September. SpaceX entered into an agreement with EchoStar (SATS) to acquire its wireless radio spectrum resources for approximately $17 billion to upgrade its cellular Starlink services. The transaction is expected to close by November 30, 2027, allowing SpaceX to assume EchoStar’s obligation to pay approximately $2 billion in cash interest on its debt. Filings indicate that while SpaceX has the option to complete the acquisition early, it would incur significantly higher costs.

Last autumn, SpaceX CEO Elon Musk stated that realizing this service requires a “roughly two-year timeframe.” He noted that the primary challenges are twofold: first, smartphone manufacturers must complete hardware adaptations to integrate EchoStar spectrum chips supporting the 1.9GHz and 2GHz bands; second, SpaceX must launch next-generation satellites capable of utilizing this additional spectrum. This includes a proposed new constellation of 15,000 satellites currently awaiting FCC approval.

Achieving 5G-Level Direct-to-Cell by 2027 with a 100-Fold Capacity Increase

SpaceX currently offers its first-generation cellular Starlink service in the U.S. through a partnership with T-Mobile US (TMUS). While this technology provides essential data connectivity—including video calling, messaging, and app access—in areas with weak cellular coverage, its available bandwidth remains limited.

In contrast, the planned second-generation cellular Starlink system is expected to deliver a connection experience approaching that of terrestrial 5G networks. In technical documents, SpaceX pointed out that the total capacity of the next-generation system will be more than 100 times greater than that of the first-generation network, with data throughput capabilities increasing by over 20 times.

David Goldman, SpaceX’s Vice President of Satellite Policy, along with two other executives, stated in the filing:

“But this is just the beginning: SpaceX has invested in spectrum resources that will allow it to launch a substantially enhanced second-generation direct-to-device system in 2027.”

This statement suggests that the company is shifting its resources and focus toward the second-generation system. The new generation is anticipated to achieve significant breakthroughs in coverage, connection speed, and system capacity, aiming to align satellite communication services with the performance of terrestrial mobile networks.

If this rollout proceeds as planned, it will strengthen SpaceX’s competitive advantage in the satellite communications market and pose a direct challenge to both traditional telecommunications providers and emerging low-Earth orbit (LEO) constellation operators. As the 2027 window approaches, the progress of spectrum integration and system R&D will remain the critical variables determining the success of this strategy.

On the morning of January12, U.S. markets once again demonstrated the growing investor interest in space-related equities. Space economy names like Planet Labs (NYSE: PL ), EchoStar Corporation (NASDAQ: SATS ), and Rocket Lab (NASDAQ: RKLB ) pushed higher, with intraday moves of +8%, +5%, and +2% respectively. This performance highlights the ongoing narrative that space technology is not only a scientific frontier but an increasingly significant theme in public markets — from satellite data services to launch solutions to space communications infrastructure. Below is a comprehensive, finance-centric analysis covering the most recent fundamental developments, business strategies, revenue and product updates, market drivers, and operational milestones for these three key space equities.

Planet Labs PBC (NYSE: PL) — Earth Imaging and Data Analytics Powerhouse

PL stock price & recent performance: Planet Labs continues to capture attention as one of the most dynamic pure-play space technology stocks. Common price figures indicate that PL stock price has traded in the low-to-mid $20s range recently, reflecting both deep volatility and renewed buying interest tied to operational progress and data revenue growth. Available financial snapshots show its revenue (TTM) at around $282M, with a market capitalization over several billion dollars, though the company remains unprofitable on a GAAP basis with negative net income and profit margins.

Business Model and Revenue Trajectory

Planet Labs occupies a unique niche as the operator of one of the largest commercial Earth-imaging satellite constellations — including fleets of “Dove” CubeSats and high-resolution Pelican satellites. The company’s core revenues derive from data licensing, subscription services, and analysis solutions tailored to sectors such as agriculture, government defense, climate monitoring, environmental tracking, and commoditized machine-learning data workflows.

Financial trend data shows consistent revenue growth: from about $291M in 2023 to higher figures in 2024 and ongoing growth in 2025, indicating double-digit year-over-year increases. TTM revenue figures suggest a clear upward path, albeit from a modest base relative to some larger aerospace peers.

Free Cash Flow and Profitability Signals

While Planet Labs has historically posted net losses and operated with a negative profit margin, recent quarterly results reveal encouraging signs: it reported multiple consecutive quarters of positive free cash flow. One earnings beat showed zero net loss against expectations of a modest loss, with revenue above forecasts and a tripled backlog, suggesting stronger demand for its data services.

The company also possesses a significant cash balance (hundreds of millions of dollars) and, importantly, levered free cash flow turning positive. This mix improves resilience in a high-capex business where satellite deployment and refresh campaigns are costly.

Contracts, Partnerships, and Product Roadmap

Recent developments point to tangible business momentum:

Planet has expanded government and defense contracts, including notable awards for global monitoring systems and integration with AI-enabled solutions under programs such as the NGA’s Luno B initiative.

The company launched advanced satellites, including hyperspectral units like Tanager-1 to detect greenhouse gases and multiple Pelican high-resolution units.

A multi-year $230M pact with SKY Perfect JSAT for building and operating a dedicated constellation underscores its strategic footprint in both commercial and international markets.

Plans to double satellite manufacturing capacity via a new Berlin facility signal a deliberate scaling of production capability.

These developments suggest PL is progressing beyond simple imagery business into AI-enhanced analytics solutions and longer-term recurring revenue streams that reduce exposure to traditional cyclical tech volatility.

Risks and Operational Challenges

While the backdrop is constructive, Planet Labs’ path encompasses notable risks:

Continual capital expenditures for constellation upgrades remain meaningful, and balancing capex with operating cash flow will be critical.

Profitability on a GAAP basis remains elusive even as free cash flow improves.

Technological competition in hyperspectral and real-time imaging (including cloud-penetrating sensors) compels ongoing R&D expenditures.

In sum, PL stock reflects a growth-oriented space data enterprise with balancing acts between expansion, cash burn, and evolving revenue quality — yet with clear fundamental improvements compared to earlier years.

EchoStar Corporation (NASDAQ: SATS) — Satellite Communications and Asset Monetization

SATS stock price & performance: Recent trading activity and financial aggregation point to EchoStar stock price around the low-hundreds (e.g., ~$121+). The stock has seen significant long-term gains, including a substantial multi-hundred-percent rally driven by strategic moves in spectrum monetization and repositioning of its business segments.

Business Evolution and Revenue Profile

EchoStar’s historical core has been satellite communications, TV distribution, broadband services, and related infrastructure. Over decades, the company has built multi-layered revenue streams including wireless, managed networks, satellite gear, and legacy pay-TV subscriber services.

Financial numbers suggest total annual revenue surpassing $15B on a trailing basis, supported by diversified business units such as wireless and broadband services. These segments provide scale relative to many space peers.

However, profitability metrics show operational and net losses in recent periods, reflecting continued investment in infrastructure and the effects of legacy business declines such as satellite TV churn. Metrics such as a negative net income margin and negative return on equity highlight the transitional phase of the business.

Strategic Pivot: Spectrum and Capital Allocation

A critical recent catalyst for SATS stock big rise is EchoStar’s aggressive monetization of its underutilized spectrum assets:

Multi-billion-dollar spectrum sales to carriers including AT&T and SpaceX have reshaped the asset profile and created significant liquidity.

These transactions have enabled EchoStar to debt-retire and reposition capital into growth areas while reducing reliance on declining legacy segments.

This strategic pivot has been large enough in scope to decouple the stock’s valuation from conventional metrics, where the rising market cap reflects perceived asset value and future growth potential.

Market and Product Development

EchoStar continues to invest in connectivity:

Expanding wireless network coverage and subscriber base through Boost Mobile and related services.

Strengthening enterprise managed solutions via HughesNet & HughesON portfolios.

Exploring 5G and satellite LEO broadband integrations that could underpin long-term service revenue.

Partnering with providers on satellite constellations and next-generation 5G connectivity.

These initiatives illustrate EchoStar’s shift toward high-growth, network-integrated space communications versus simple broadcast distribution.

Risks and Structural Considerations

Despite asset strength, challenges persist:

Core operational profitability has materially lagged, influencing lower traditional valuation multiples.

Integration risks around spectrum monetization and regulatory hurdles (including FCC requirements) pose execution complexity.

Ongoing legacy segment declines require careful balancing of resources with growth business needs.

In broader terms, SATS stock presents a unique case where equity performance is driven by asset redeployment and balance sheet repositioning, rather than conventional top-line or EPS momentum.

Rocket Lab USA (NASDAQ: RKLB) — Launch Services and Space Systems Integrator

RKLB stock price & performance: Rocket Lab’s RKLB stock price has traded in volatile ranges but has notably surged significantly year-over-year, with trading levels in the $50+ range recently. This reflects market enthusiasm around strategic milestones, backlog growth, and the company’s expanding role in launch and space systems.

Financial Metrics and Growth Trajectory

Rocket Lab’s strategy blends orbital launch services (Electron) with forward-looking products such as the Neutron medium-lift rocket and satellite systems manufacturing.

Recent earnings data have shown high single-to-mid-double-digit revenue growth (30%-50%+ YoY), with quarterly revenues near ~$150M in Q3 2025. This puts RKLB well above the sector median growth rate, signaling meaningful commercial scaling.

Full-year financial results from earlier periods demonstrate structural momentum — record launches, expanded contract wins, and year-over-year top-line gains.

Product Development — Electron and Neutron

Electron has established Rocket Lab as a key leader in dedicated small-satellite launch services. Its frequent launches and precision placement have driven a growing backlog and diversified customer base across commercial and defense segments.

The Neutron rocket represents a major strategic inflection point — offering medium-lift capability and reusable architecture, potentially enabling Rocket Lab to compete more directly with larger players for constellation deployment missions. This product’s development progress has been cited as a primary valuation driver and a key reason behind elevated RKLB stock big rise narratives.

Backlog and long-term contracts, including defense work and multi-launch commitments for future constellations, provide revenue visibility well into the next decade.

Risk Profile and Competitive Dynamics

No less than other space companies, Rocket Lab faces execution and financial challenges:

R&D and infrastructure investments (especially for Neutron) remain high, delaying consistent profitability in the near term.

Competition from incumbents like SpaceX may compress launch pricing and constrain market share expansion.

Operational milestones and launch schedule adherence are materially tied to investor sentiment and share price volatility.

Conclusion: Sector Context and Strategic Themes

The performance of PL, SATS, and RKLB around December 13 reflects broader investor enthusiasm for the space economy theme — one anticipated to expand from hundreds of billions to potentially trillions of dollars by the 2030s as data services, connectivity, launch solutions, and space infrastructure converge.

Each company offers a distinct vantage point:

Planet Labs leverages its satellite network and data analytics to build recurring revenues and AI-enhanced services.

EchoStar pivots from legacy broadcast models to asset monetization and network-agnostic space communications.

Rocket Lab positions itself as a full-stack launch and space systems provider with growth tied to emerging next-generation rocket platforms.

Despite positive momentum, all three stocks remain subject to macroeconomic influences, capital expenditure cycles, R&D intensity, and execution risk — underscoring why space stocks are both high-growth and high-variance narratives in public markets today.