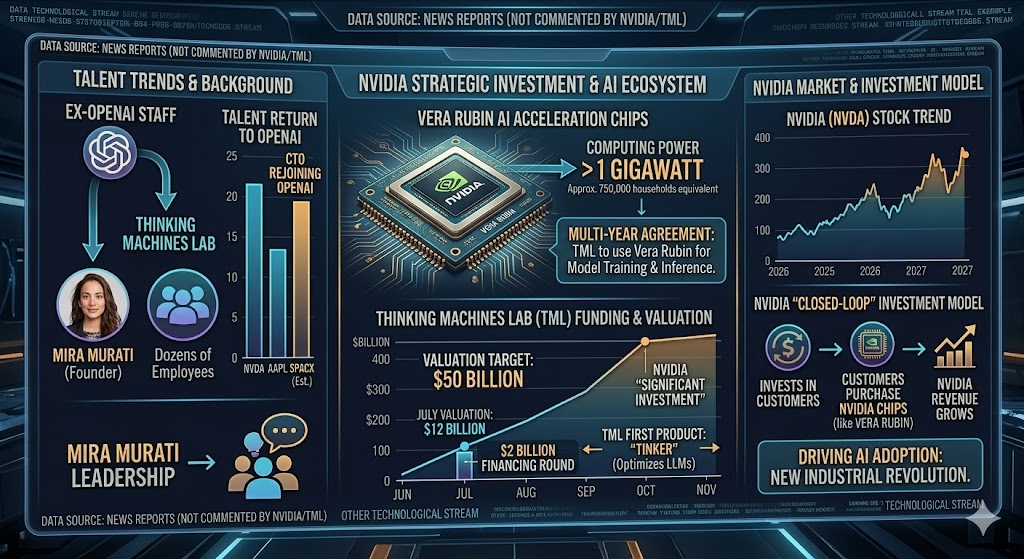

Nvidia has announced a new round of investment in Thinking Machines Lab, an artificial intelligence (AI) company founded by former OpenAI executive Mira Murati, and will provide the startup with chips to train and run its AI models.

Both companies stated in a press release on Tuesday that, under a multi-year agreement, Thinking Machines Lab will use Nvidia’s upcoming Vera Rubin AI acceleration chips. These chips are expected to be deployed early next year and will provide Thinking Machines Lab with at least 1 gigawatt of computing power (equivalent to the electricity consumption of approximately 750,000 households).

Nvidia had previously invested in Thinking Machines Lab last year. The specific terms of this investment were not disclosed, and it was not clarified whether the funding would be in cash, chips, or a combination of both. Nvidia referred to this as a “significant investment.” A spokesperson for Thinking Machines Lab declined to provide further details, and Nvidia has not yet responded to requests for comment.

As the world’s most valuable company, Nvidia has been involved in a series of investment deals in recent months. The chip giant is leveraging its resources to drive AI adoption across various industries and help fuel what it describes as a “new industrial revolution.” However, these investments have drawn attention due to the closed-loop nature of the model—Nvidia is investing in its own customers.

According to reports from November of last year, Thinking Machines Lab had been seeking a new round of funding, targeting a valuation of $50 billion. If achieved, this would represent a fourfold increase from its previous valuation of $12 billion in July, when the company completed a $2 billion financing round at that valuation.

Murati stated in a press release, “This partnership will accelerate our goal of building AI that users can truly shape and own, which will, in turn, unlock human potential.”

Murati, who previously served as OpenAI’s Chief Technology Officer, has led Thinking Machines Lab to recruit dozens of employees from OpenAI. The company launched its first product, Tinker, in October of last year. Tinker is designed to help users optimize large language models—this is the underlying technology behind chatbots like ChatGPT.

However, in recent months, Thinking Machines Lab has faced talent return, with several employees, including its CTO, rejoining OpenAI.