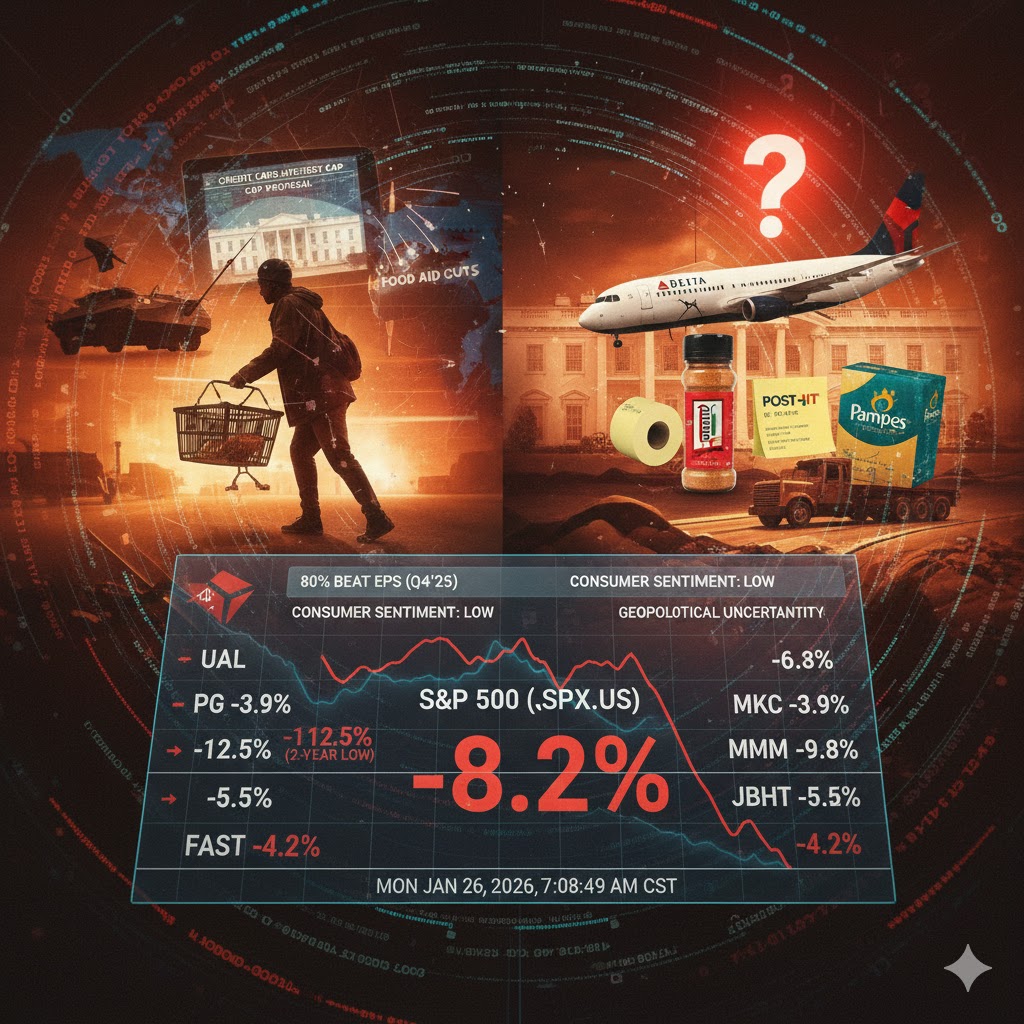

As the U.S. earnings season gathers pace, corporate executives are issuing a collective warning about the consumer outlook. Despite economic data showing steady growth, CEOs across sectors—from aviation and consumer goods to industrial fields—report that geopolitical tensions and policy uncertainties are making consumers cautious and corporate planning increasingly difficult.

Several industry leaders released cautionary signals in their latest reports. Delta Air Lines (DAL) maintained a guarded stance on profits amid geopolitical instability, while United Airlines (UAL) warned that global tensions could dampen travel demand. Executives at Procter & Gamble (PG) and McCormick (MKC) noted that consumers are remaining prudent. 3M (MMM) saw its sharpest decline since April after its outlook fell short of expectations, citing an uncertain macro environment for its consumer and automotive businesses. Similarly, results from industrial distributor Fastenal (FAST) and logistics firm J.B. Hunt (JBHT) left investors disappointed.

These pessimistic notes contrast with many key economic indicators. Data from last year showed steady growth and resilient consumer spending. According to Bloomberg Intelligence, as of Thursday’s close, 80% of S&P 500 companies that have reported results exceeded analyst expectations.

Corporations are reporting at a rare intersection of political upheaval and global uncertainty. With the S&P 500 Index (.SPX) posting double-digit gains for three consecutive years, stock valuations are high, leaving little room for error. Executives now face the difficult task of setting the tone for the coming year as President Trump continues to reshape U.S. trade relations and international policy.

Corporate America Warns of Early-Year Growth Pressure

United Airlines noted that U.S. military actions in Venezuela have had a “measurable negative impact” on Caribbean bookings. CEO Scott Kirby warned that geopolitical risks could disrupt what otherwise appeared to be a strong start to the year.

The Chicago-based carrier also pointed to a larger-than-expected blow from President Trump’s proposed credit card interest rate cap. This reflects the deep ties between airlines and the payment industry through lucrative co-branded card partnerships—a proposal that caused financial stocks to tumble earlier in the earnings season.

Meanwhile, consumer goods giants are feeling the squeeze. McCormick (MKC) CEO Brendan Foley stated during a Thursday call: “The environment in our key markets is characterized by volatility and continues to face pressures from inflation, geopolitical and trade uncertainties, and the risk of rising unemployment. Overall consumer confidence remains low.” The spice and condiment maker saw its shares suffer their biggest drop in two years as both Q4 results and full-year guidance missed targets.

Procter & Gamble, the maker of Pampers and Tide, noted similar disruptions despite forecasting sales growth for the next six months. Both P&G (PG) and McCormick cited the temporary halt of food assistance programs (SNAP) due to the government shutdown as a blow to low-income consumers, which in turn impacted sales.

Industrial firms noted lingering demand headwinds. The CFO of Fastenal remarked that the U.S. economy “continues to send mixed signals, particularly in the industrial sector.” At J.B. Hunt, executives said the freight market remained unstable at the start of the year—even as immigration policy restricted labor supply, a dynamic that usually supports higher shipping rates.

3M ($MMM.US) saw its stock price hit the largest drop since April after releasing a lower-than-expected outlook. The manufacturer of Post-it notes, roofing granules, and electronic materials stated that the macro environment for its consumer and automotive businesses remains uncertain.

Policy Uncertainty Dominates Corporate Planning

Steve Sosnick, Chief Strategist at Interactive Brokers (IBKR), said policy uncertainty is “absolutely” overshadowing positive corporate news:

“It really makes it harder for management to plan… but what CEO is going to say, ‘White House policy instability is making it hard for me to run my business’?”

Corporations are releasing results at a rare junction of political turmoil and global uncertainty. The challenge for CEOs is how to define the company’s future outlook against the backdrop of Trump’s continuous reshaping of trade relations and international policies.

Meanwhile, parts of the Trump policy agenda could provide near-term relief for consumers. Investors are betting that excess tax refunds and potential stimulus measures might help bolster spending for low-income households, at least temporarily. The White House has placed affordability at the core of its messaging, from credit card interest initiatives to efforts to force tech companies to bear rising electricity costs.

Eric Clark, Chief Investment Officer at Accuvest Global Advisors, noted:

“This is a mid-term election year, so the rhetoric has started. Who knows if it actually helps the consumer? But it might make them feel like help is on the way, which ultimately helps boost sentiment.”

The aviation industry has long been considered a high-stakes barometer for the global economy, and the January 13 release of the DAL Financial Report for the fourth quarter and full year of 2025 has provided the most definitive reading yet of the “new normal” in air travel. Delta Air Lines(DAL), the Atlanta-based titan of the skies, unveiled a set of results that reflect a company operating at two different speeds: a record-shattering engine of high-margin premium services and a domestic segment still nursing the bruises of political and economic instability.

On the day of the announcement, the DAL stock price exhibited a classic “sell-on-news” reaction, tumbling 3.56% to close at $69.33. This dip occurred despite the airline reporting a significant beat on its bottom line, with an adjusted earnings per share (EPS) of $1.55 against a consensus forecast of $1.52. The market’s hesitation stems not from the past year’s performance—which was by many accounts the best in the company’s history—but from a cautious outlook regarding a 2026 landscape where labor costs are rising and the “K-shaped” recovery is creating a widening chasm between luxury and leisure travel. To understand the future of Delta Air Lines stock, one must look beyond the immediate turbulence and into the structural transformation of its revenue engine.

Record Revenues and the $200 Million Shutdown Shadow

The headline story of the Delta Air Lines Earnings for 2025 is one of unprecedented scale. The carrier achieved record annual adjusted revenue of $58.3 billion, a 2.3% increase year-over-year. For the full year, Delta generated a pre-tax income of $5 billion and an operating margin of 10%. These figures represent the “fortress” of the Delta business model, which has consistently outperformed its peers in profitability and operational reliability.

However, the fourth quarter brought a specific challenge that tested this resilience: a 43-day U.S. government shutdown in late 2025. This geopolitical friction caused a direct $200 million hit to Delta’s revenue, primarily in the domestic segment where federal travel and government-related business evaporated during the standoff. This disruption was a major factor in the slight revenue miss for Q4, where adjusted operating revenue came in at $14.6 billion—just shy of the $14.72 billion analysts had penciled in.

Despite this headwind, the bank-like stability of Delta’s loyalty and premium programs provided a vital cushion. Revenue from diversified streams—including the lucrative American Express partnership, Cargo, and Maintenance, Repair, and Overhaul (MRO) services—now accounts for 60% of Delta’s total revenue. This shift is critical for the long-term valuation of DAL stock, as these high-margin, less-cyclical business lines reduce the company’s traditional dependence on the volatile “Main Cabin” leisure market.

The Premium Pivot: Catering to the Affluent Flyer

The most striking trend within the DAL Financial Report is the divergence in passenger behavior. While the “Main Cabin” revenue has remained relatively stagnant, reflecting the affordability constraints of the middle-class traveler, premium revenue surged by 7% year-over-year. Delta is no longer just an airline; it is a luxury hospitality provider that happens to operate aircraft.

This “Premium Advantage” is at the heart of Delta’s 2026 strategy. The airline is aggressively expanding its “Delta One” and “Premium Select” offerings, catering to a demographic that appears immune to inflationary pressures. This strategy is not merely about comfort; it is about yield management. By filling the front of the plane with high-paying customers, Delta can maintain double-digit margins even if it has to discount seats in the back to maintain load factors.

The numbers support this aggressive positioning. Delta’s unit revenue premium relative to the industry reached nearly 115% in 2025. This means that for every dollar a competitor earns per seat, Delta is earning $1.15. This premium is driven by a combination of superior operational reliability—Delta was recognized as the most on-time airline in the U.S. for the fifth consecutive year—and a loyalty program that continues to grow. Remuneration from the American Express partnership grew 11% to $8.2 billion in 2025, and management expects this to reach $10 billion within the next few years.

Fleet Modernization: The 787 and A350 Strategic Mix

A significant portion of the Delta Air Lines Earnings discussion centered on the company’s capital allocation and fleet strategy. On the day of the earnings release, Delta confirmed a landmark order for 30 Boeing 787-10 Dreamliners, with options for 30 more. This move is a strategic masterpiece of diversification. For years, Delta has been heavily reliant on Airbus for its widebody needs, with a large fleet of A350s and A330neos. By adding the 787-10 to its arsenal, Delta is not only securing better pricing through competition but is also optimizing its fleet for different route profiles.

The Airbus A350-1000s, which will begin arriving in 2026, are designed for the longest-haul international routes, while the Boeing 787-10s offer exceptional fuel efficiency for high-demand transatlantic and transpacific corridors. Fuel efficiency is a primary driver of the long-term bull case for DAL stock. The A350, for example, burns 25% less fuel per seat than the older aircraft it replaces. In an era of volatile energy prices and increasing carbon taxes, a younger, more efficient fleet is a massive competitive advantage.

Delta’s reinvestment in its fleet reached $4.3 billion in 2025, yet the company still managed to generate record free cash flow of $4.6 billion. This “cash machine” status is what allows Delta to simultaneously modernize its fleet and aggressively pay down debt. Adjusted net debt was reduced by $3.7 billion over the course of the year, bringing the gross leverage down to a healthy 2.4x. This strengthening of the balance sheet is essential as Delta enters a 2026 fiscal year where it will transition to becoming a partial taxpayer, a move that will put more focus on pre-tax earnings growth.

Labor Costs and the Margin Squeeze

If there is a “dark cloud” in the DAL Financial Report, it is the persistent rise in operating expenses. Total operating expenses for the fourth quarter increased by 5% to $14.5 billion. The primary driver? Salaries and related costs, which jumped 11% to $4.6 billion. The airline industry is currently in a “labor-positive” cycle, where pilots, flight attendants, and ground crews have significant bargaining power.

Delta has chosen to lead with generosity, awarding a 4% pay increase in 2025 and announcing a $1.3 billion profit-sharing payout for its employees this February. While this “people-first” culture is a pillar of Delta’s brand, it creates a high fixed-cost base that could be problematic if revenue growth slows. Management has guided for 2026 non-fuel unit costs (CASM-Ex) to grow in the “low-single digits,” a target that many analysts find ambitious given the current wage environment.

The market’s reaction to the DAL stock price on January 13 reflects this concern. Investors are questioning whether the 10% operating margin is a ceiling or a floor. If Delta can continue to grow its premium revenue at 7-10% while keeping labor cost growth below 5%, the margin expansion story remains intact. If labor costs spiral, however, the bank-like earnings of the airline could be at risk.

Expanding the Frontier: The 2026 International Strategy

While the domestic market faces “K-shaped” friction, Delta’s international segment is poised for an explosive 2026. The airline has announced its largest-ever transatlantic summer schedule, with over 650 weekly flights. New routes, such as New York-JFK to Riyadh and Los Angeles to Hong Kong, signal a strategic push into high-yield business and tourism markets that were previously underserved.

The partnership with Riyadh Air and the expansion in the Northeast and West Coast hubs (Boston and Seattle) are designed to capture a larger share of the global corporate travel market. Recent corporate surveys cited in the Delta Air Lines stock analysis indicate that 90% of companies expect their travel volume to either increase or remain steady in 2026. This is a critical tailwind, as corporate travelers typically book the high-margin premium cabins that drive Delta’s profitability.

Furthermore, Delta is leveraging technology to maximize this international expansion. The near-completion of fast, free Wi-Fi across the mainline fleet (95% coverage by the end of 2025) and the use of AI-powered pricing optimization tools are expected to drive incremental revenue gains. Management’s outlook for 2026 includes a revenue growth of 5-7% for the March quarter, which is several points ahead of projected capacity growth—a clear sign of pricing power.

Market Sentiment and Technical Price Outlook

The current valuation of DAL stock presents a fascinating puzzle for value investors. Trading at a price-to-earnings (P/E) ratio of approximately 9.7x, Delta is significantly cheaper than the broader S&P 500 and even many of its industrial peers. This low multiple suggests that the market is still pricing in the cyclical risks of the airline industry, rather than the stable, fee-based revenue streams that Delta has built.

From a technical perspective, the DAL stock price is currently testing support in the $68-$70 range. This area has historically been a zone of strong buying interest. The 52-week high of $73.16 remains the primary resistance level. If the stock can break above this on the back of a strong Q1 2026 performance, a path toward $85.00—the price target set by several leading analysts—becomes increasingly likely.

However, investors must remain cognizant of the macro environment. Any further domestic political instability or a significant spike in oil prices would put immediate pressure on the Delta Air Lines stock. Currently, Delta is benefiting from lower-than-expected fuel prices, with an adjusted average price of $2.28 per gallon in Q4. If this were to climb back toward $3.00, the 20% EPS growth target for 2026 would be difficult to hit.

The Long-Term Horizon: A 20% Growth Target

The most ambitious part of the DAL Financial Report was the guidance for the full year 2026. Management expects to deliver margin expansion and earnings growth of 20% year-over-year, with EPS ranging from $6.50 to $7.50. This is a bold statement in an industry that is notoriously unpredictable.

The confidence behind this 20% target stems from three factors:

Normalization of Domestic Travel: As the impact of the 2025 government shutdown fades, domestic revenue is expected to rebound.

Accretive Premium Growth: The continued roll-out of Premium Select and Delta One lounges will drive higher yields.

Efficiency Gains: The retirement of older, less-efficient aircraft in favor of A350s and 787s will lower the unit cost of operation.

For those holding Delta Air Lines stock, 2026 will be the year that determines whether Delta has truly broken the “boom-and-bust” cycle of the airline industry. If the company can deliver on its $3 billion to $4 billion free cash flow target while maintaining its premium pricing power, the current P/E of 9x will look like a historic anomaly.

Conclusion: Flying Above the Fray

The January 13 DAL Financial Report paints a picture of a company that is masterfully navigating a complex global landscape. By pivoting toward premium services, diversifying its revenue through loyalty and MRO, and modernizing its fleet with surgical precision, Delta Air Lines has created a business model that is more resilient than ever.

While the immediate DAL stock price may be subject to the whims of quarterly sentiment and short-term macro shocks, the underlying fundamentals of the “Delta Fortress” remain strong. The record $58.3 billion in revenue and the $4.6 billion in free cash flow are not just numbers; they are proof of a strategy that is working. As we move into the 2026 travel season, the focus will remain on whether Delta can translate its operational excellence into the 20% earnings growth it has promised. In the high-altitude world of global aviation, Delta continues to fly in a class of its own.