As the global financial architecture navigates the complexities of early 2026, JPMorgan Chase stock stands as the definitive benchmark for banking resilience and innovation. Under the steadfast leadership of Jamie Dimon, the firm has not only weathered the “policy storm” of 2025 but has accelerated its transformation into a technology-first financial utility. For institutional allocators and individual market participants tracking the JPM stock price, the current market landscape reflects a company that has successfully decoupled its growth from traditional interest rate cycles, leaning instead into an AI-driven “operational alpha” and a relentless global expansion strategy.

The Quantitative Core: Deconstructing the 2025 Financial Performance

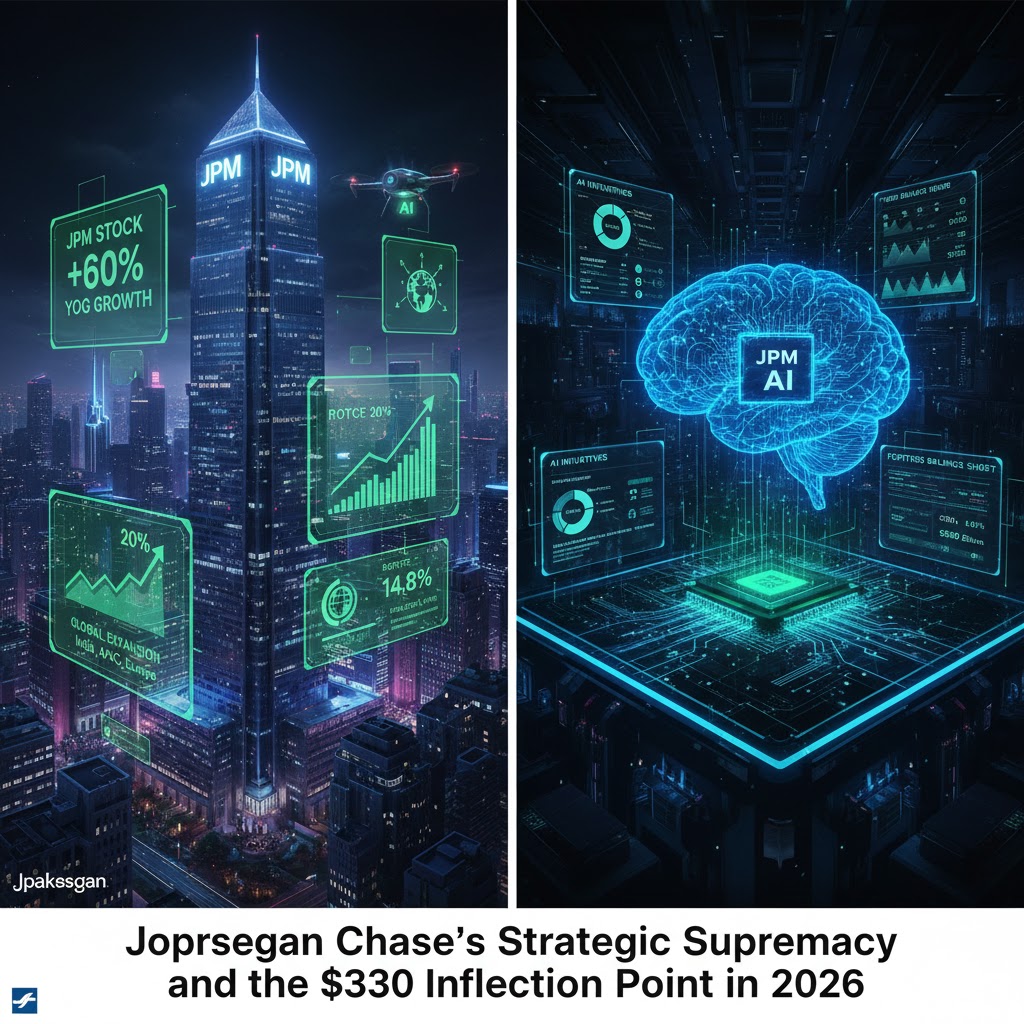

JPMorgan Chase & Co. (NASDAQ: JPM) entered 2026 coming off a fiscal year that silenced critics of the “high-for-longer” fallout. The firm’s third-quarter 2025 earnings report set a historic tone, with net income surging 12% year-over-year to $14.4 billion, or $5.07 per share. This performance was underpinned by a robust 9% increase in total revenue, which reached $47.1 billion, far exceeding analyst consensus.

Crucially, the bank’s Return on Tangible Common Equity (ROTCE) hit 20% in the latter half of 2025, a figure that places it at the apex of the global G-SIB (Global Systemically Important Banks) list. While Net Interest Income (NII) showed early signs of stabilization as the Federal Reserve initiated a measured easing cycle, the bank’s non-interest income—driven by Markets, Payments, and Asset Management—filled the gap with double-digit growth. For those analyzing JPM stock, the most significant takeaway is the fortress balance sheet: a CET1 ratio of 14.8% and a total loss-absorbing capacity exceeding $568 billion as of late 2025.

The market’s reaction to these fundamentals has been decisive. As of January 9, 2026, the JPM stock price closed at $329.28, having recently touched an all-time high of $337.25 earlier in the week. This represents a staggering 52-week appreciation of over 60% from its lows of $202.16. With a market capitalization now exceeding $910 billion, JPMorgan Chase is knocking on the door of the $1 trillion club, a milestone previously reserved for the tech-heavy “Magnificent Seven.”

The AI Supercycle: From Aspirations to Tangible Economic Impact

If 2024 was the year of AI experimentation, 2026 is the year of AI integration for JPMorgan. The bank’s “AIP-first” (AI Platforms) strategy has moved beyond back-office automation into front-end client services and risk management. JPMorgan’s 2026 Action Plan allocates over $17 billion to technology, with a significant portion dedicated to private cloud infrastructure and custom LLM (Large Language Model) deployment.

The bank’s proprietary “IndexGPT” and “Spectrum AI” tools are now fully operational within the Commercial & Investment Bank (CIB) division. These tools have reportedly reduced the time required for complex debt issuance structuring by 40%, allowing the firm to capture a larger share of the rebounding M&A and IPO market. In the Consumer & Community Banking (CCB) segment, AI-driven personalized financial advice has increased customer retention rates by 150 basis points, a critical metric for long-term deposit stability.

Investors in JPMorgan Chase stock are increasingly viewing these technological advancements as a “yield enhancer.” By driving the cost of financial expertise toward zero, JPMorgan is effectively expanding its net interest margins through operational efficiency rather than just rate spreads. The firm anticipates that AI-driven productivity gains could contribute between $1.5 billion and $2 billion to the bottom line by the end of fiscal 2026.

Market Expansion: The New Global Frontier and Regional Dominance

While the U.S. remains the firm’s primary engine, 2026 marks a pivotal year for its international “sovereign” strategy. JPMorgan has successfully localized its digital banking platform in several key European and Asia-Pacific markets. In India, the bank’s tech hub has grown to over 60,000 employees, serving not just as a back-office support system but as a center for global product development.

Domestically, the bank’s “Middle Market Rebound” has been a central theme. Following the 2024 U.S. election, small and midsize business optimism surged, leading to an 8% year-over-year increase in average loans. JPMorgan’s ability to provide a “full-stack” solution—ranging from simple checking to complex capital raising—has allowed it to gain significant market share from smaller regional lenders who are still grappling with the regulatory fallout of the 2023 banking crisis.

Furthermore, the bank’s new global headquarters in New York City and its expanded London presence are physical manifestations of its long-term confidence. These hubs are designed to house the next generation of “Human-AI teams,” reinforcing the idea that JPMorgan Chase stock is a bet on the future of organized intelligence in finance.

2026 Strategic Outlook: Navigating Polarization and Fragmentation

As we look toward the remainder of the year, the JPM stock price will be influenced by three primary forces: geopolitical fragmentation, the trajectory of the U.S. labor market, and the “AI Lift vs. Economic Drift” dynamic. JPMorgan’s Global Research team has highlighted a 35% probability of a U.S. recession in late 2026, citing sticky inflation and slowing labor supply as potential headwinds.

However, the firm’s “Fortress Principles” are designed for exactly this type of environment. With a net payout ratio of 73% over the last twelve months and $8 billion in net repurchases in Q3 2025 alone, the bank is returning massive amounts of capital to shareholders while maintaining a liquidity cushion that allows it to be the “lender of last resort” in any market dislocation.

Key catalysts for the coming quarters include:

- The Q4 2025 Earnings Release (January 2026): Analysts expect a confirmation of robust investment banking fees as the M&A pipeline continues to clear.

- The Federal Reserve’s H1 2026 Policy Path: Two additional rate cuts are priced into the market, which would likely support equity valuations and loan demand.

- Capital Markets Re-Rating: If JPMorgan achieves its expected ROTCE of 20% for the full year 2026, several Wall Street firms, including BofA Securities and TD Cowen, have projected a price target exceeding $375 for AAPL stock.

In conclusion, JPMorgan Chase enters 2026 in its strongest competitive position in decades. By blending the raw power of its trillion-dollar balance sheet with the surgical precision of agentic AI, the bank has transcended the traditional “bank” label. It is now a global technology utility that also happens to move the world’s money. While the JPM stock price may face volatility as the market debates the timing of a potential “soft landing,” the underlying structural advantages of the firm suggest that the Fortress is only getting stronger.